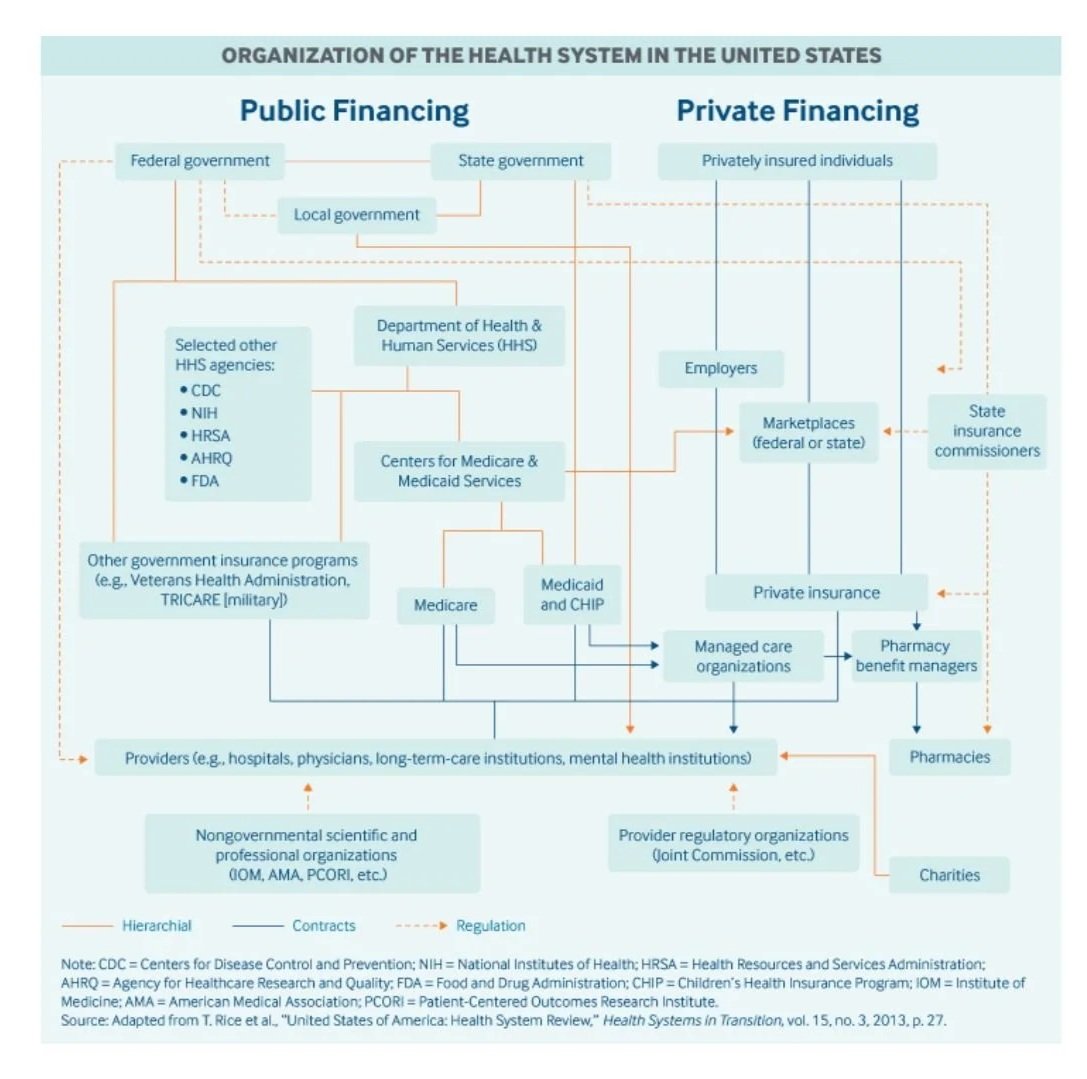

All Basics

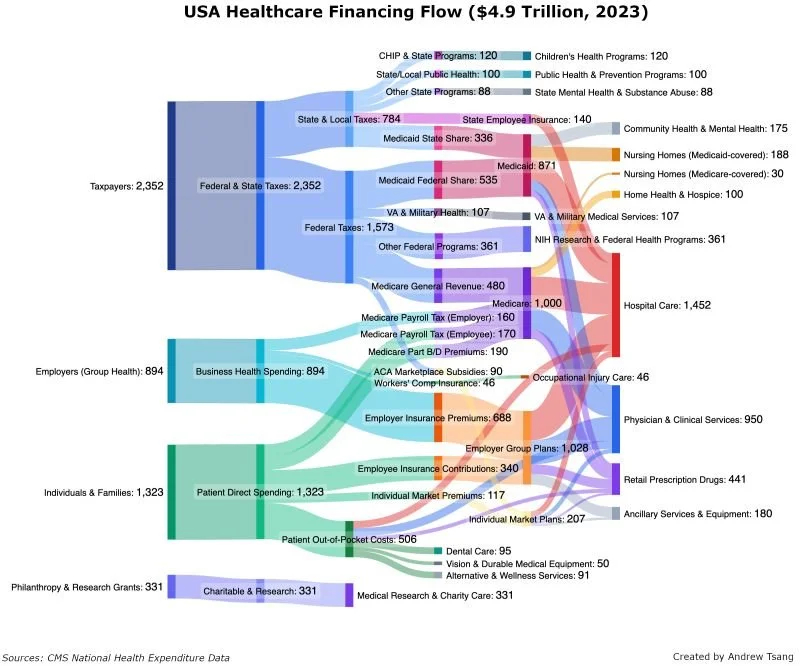

Health Insurance: Health insurance is a product, not a service. It remains the bane of everyone’s existence - physicians and patients. No one realizes how many different systems of insurance actually exist. Remember, Private pays more than Medicare which pays more than Medicaid to a physician for treating the SAME health condition (type 2 diabetes in a patient with a septic joint). We live in a system where your financial status determines the value of your health — not figuratively. Looking at the second graph by Andrew Tsang, you realize the deep connection we all have in terms of our healthcare finances. You may think you are separate from Medicaid because you pay in cash or because you have fancy employer insurance. But you indirectly or directly subsidize Medicaid, Medicare, and uninsured payments either through your taxes, salary, or your premiums itself.

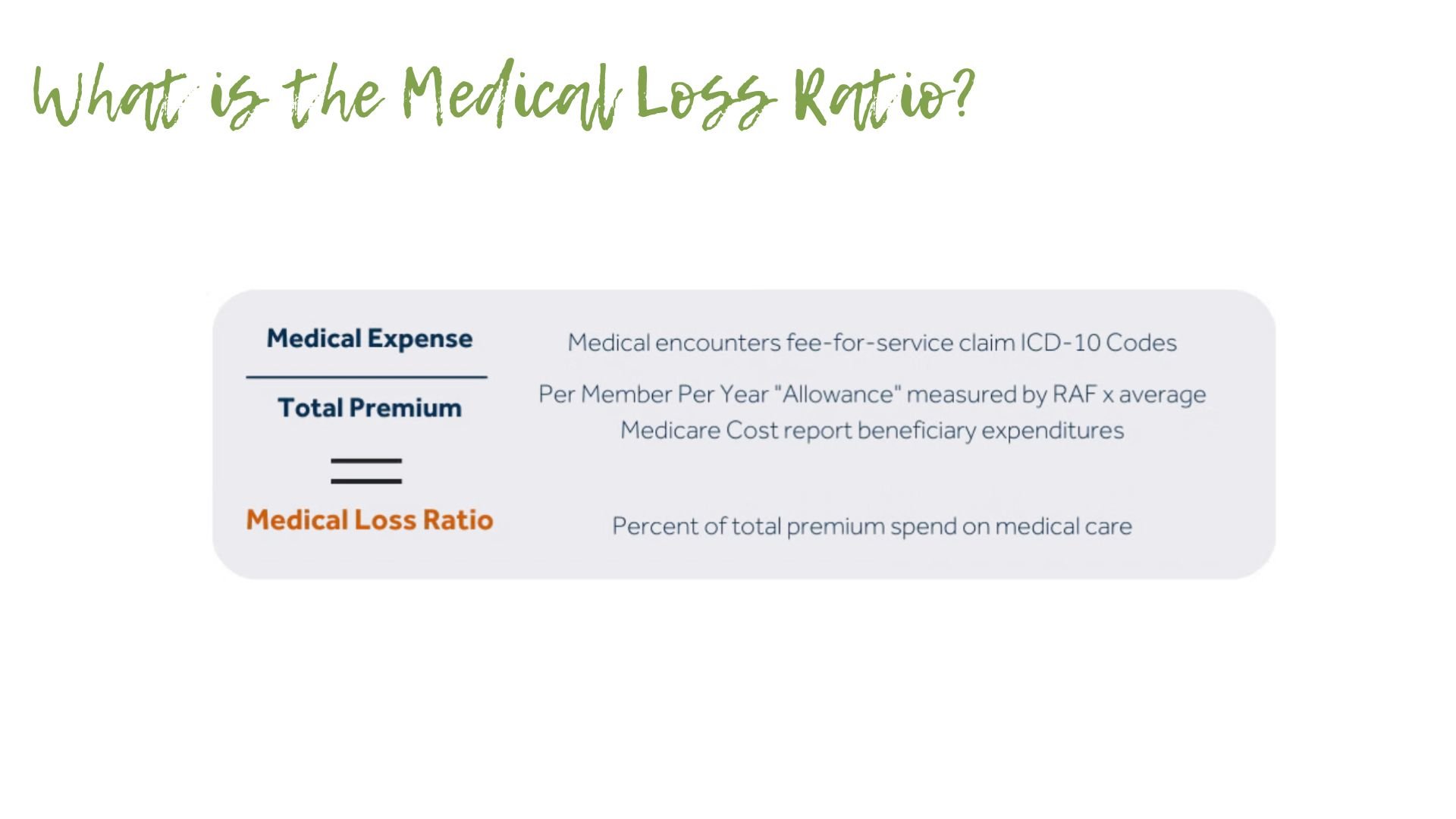

Medical Loss Ratio: The Affordable Care Act established a medical loss ratio where insurance companies have to spend 80% of their healthcare premiums (their “revenue”) on “direct medical care” as opposed to administrative costs of running the company. It is a simple formula. However, the Affordable Care Act cannot by itself cure unchecked greed. In a traditional, fee for service, fully insured model, if a health insurance company collects $500 in premiums instead of $100 in premiums…the 20% they can spend on administration still goes from $20 -> $100. 20% of a bigger pie is still bigger, even though you’re capped at 20%. So, they absolutely do not care about lowering costs in this scenario. In a later lesson, after we learn about value based care, we will see sometimes as the incentives and payment models change, the MLR actually works how President Obama intended. But, in traditional health insurance models, more premiums -> more pie -> higher 20% of pie.

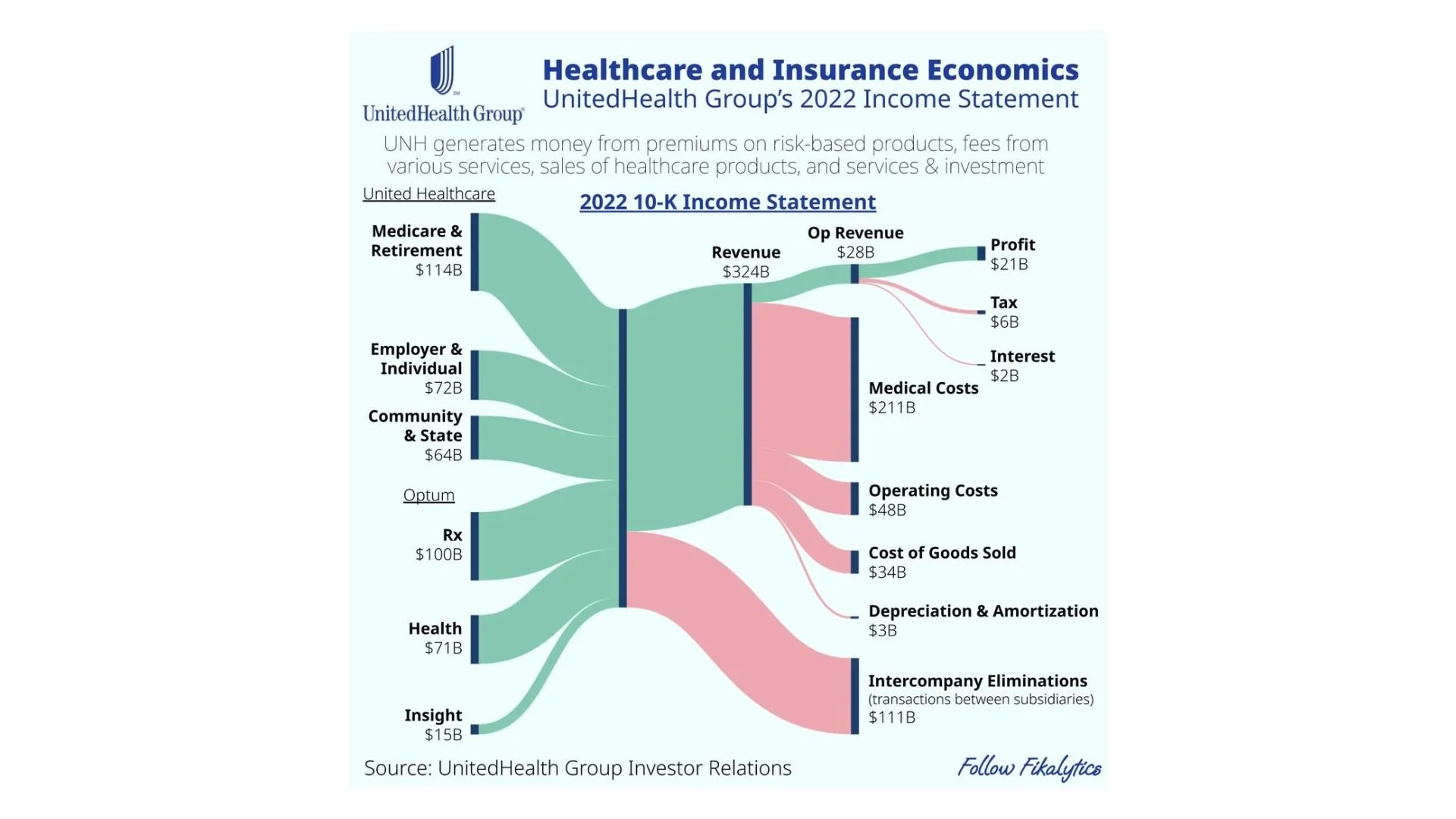

Intercompany Subisidaries: The income diagram for United Healthcare shows you how the giant insurance companies hide their money. If you look at just the premiums total (so Medicare + State + Employer), and then you look at "Medical Costs", the Medical Costs come to 84% of the total premiums. It makes it look like profit is the tiny 21B at the top. However, the "intercompany eliminations" is huge because basically everything coming from Optum gets obfuscated and it does not look like revenue or profit, even though it is.